When buying motor insurance, one of the first decisions you’ll face is whether to opt for Comprehensive Insurance or Third-Party Insurance. While both protect you financially after an accident, they differ significantly in coverage scope, cost, and applicability. A basic understanding often isn’t enough—small policy details can make a big difference in your claim experience and out-of-pocket expenses. This article dives deeply into what each type covers, what it doesn’t, and how to decide which is right for you.

Definition and Scope

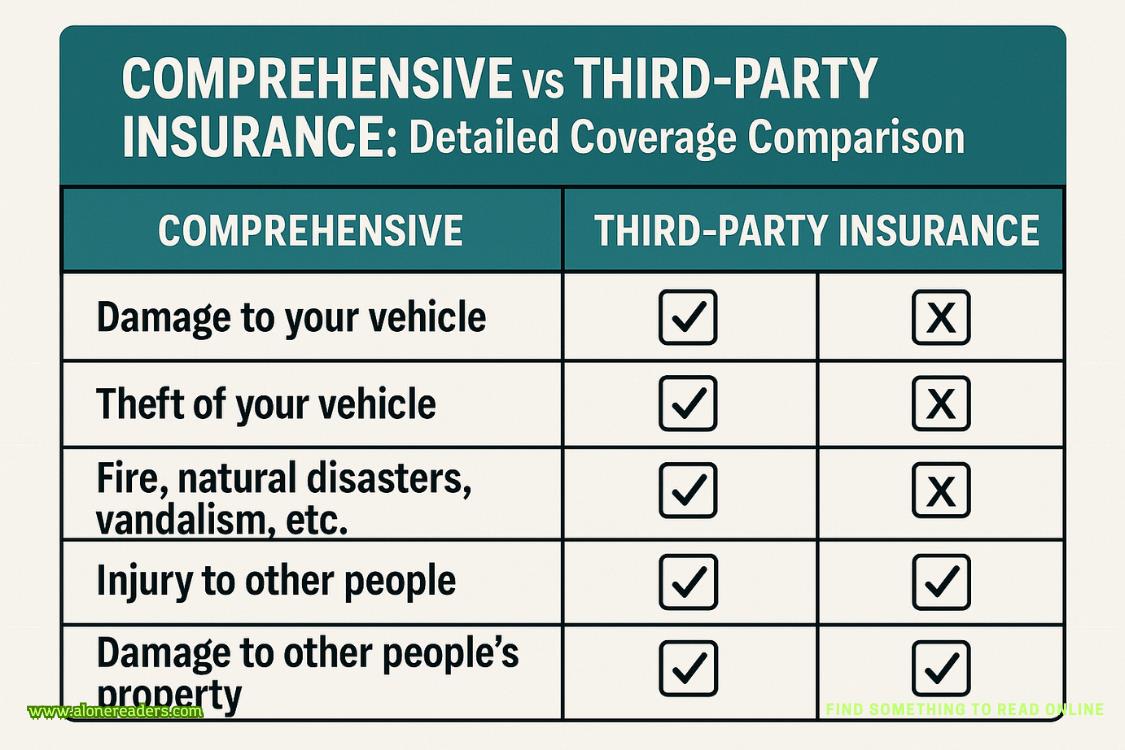

Comprehensive insurance provides the widest coverage available for vehicle owners. It covers damage to your own car, damage to third-party property, and a wide range of non-collision events. This is often referred to as “own damage + third-party” cover.

What It Covers

Key Advantages

Limitations & Exclusions

Definition and Scope

Third-party insurance is the most basic form of legally required motor insurance in many countries. It only covers damage or injury you cause to others, offering no protection for your own vehicle.

What It Covers

What It Does NOT Cover

Key Advantages

Limitations & Exclusions

| Aspect | Comprehensive Insurance | Third-Party Insurance |

|---|---|---|

| Own Vehicle Damage | Covered | Not Covered |

| Third-Party Liability | Covered | Covered |

| Theft Protection | Covered | Not Covered |

| Natural Disasters | Covered | Not Covered |

| Fire & Vandalism | Covered | Not Covered |

| Premium Cost | Higher | Lower |

| Customizable Add-ons | Yes | Limited |

| Best For | New/expensive cars, high-risk areas, or high usage | Older/low-value cars or budget-conscious drivers |

Why Comprehensive Costs More

Factors Affecting Premiums for Both Types

Choosing between comprehensive and third-party insurance should not be a decision based purely on price. Comprehensive insurance offers extensive protection, making it ideal for new or high-value vehicles and high-risk driving environments. Third-party insurance, while limited, is a cost-effective option for older cars or those seeking to meet legal requirements at the lowest possible cost.

A good rule of thumb is to weigh the replacement cost of your vehicle against the annual difference in premiums. If your vehicle’s value is significantly higher than the savings from choosing third-party coverage, comprehensive insurance usually makes better long-term sense.

October 25, 2023

January 02, 2025

Top 10 Affordable Electric Cars for 2026: Best Budget EVs Worldwide

Top 10 Affordable Electric Cars for 2026: Best Budget EVs Worldwide

Tesla Model S Review: Speed, Range, and Features in 2026

Tesla Model S Review: Speed, Range, and Features in 2026

Honda Accord vs Toyota Camry: Which Mid-Size Sedan Is Better?

Honda Accord vs Toyota Camry: Which Mid-Size Sedan Is Better?

Chevrolet Silverado vs GMC Sierra: Which Truck Wins?

Chevrolet Silverado vs GMC Sierra: Which Truck Wins?

2026 Jeep Wrangler Review: Off-Road Capabilities Tested in Extreme Terrain

2026 Jeep Wrangler Review: Off-Road Capabilities Tested in Extreme Terrain

2026 Nissan Altima Review: Tech, Comfort, and Safety – In-Depth Expert Analysis

2026 Nissan Altima Review: Tech, Comfort, and Safety – In-Depth Expert Analysis

Colonial Competition in North America: France vs England

Colonial Competition in North America: France vs England

French Exploration in North America: Jacques Cartier and Samuel de Champlain

French Exploration in North America: Jacques Cartier and Samuel de Champlain

The Dutch-Portuguese War: Battle for Trade Routes in Asia and Africa

The Dutch-Portuguese War: Battle for Trade Routes in Asia and Africa

The Spanish Armada (1588): Naval Warfare and the Shift in European Power

The Spanish Armada (1588): Naval Warfare and the Shift in European Power

The Reign of Sweyn Forkbeard: How Denmark Became a North Sea Power

The Reign of Sweyn Forkbeard: How Denmark Became a North Sea Power

Famous Viking Warriors and Leaders: Ragnar Lothbrok, Ivar the Boneless, and Other Legendary Norse Heroes

Famous Viking Warriors and Leaders: Ragnar Lothbrok, Ivar the Boneless, and Other Legendary Norse Heroes

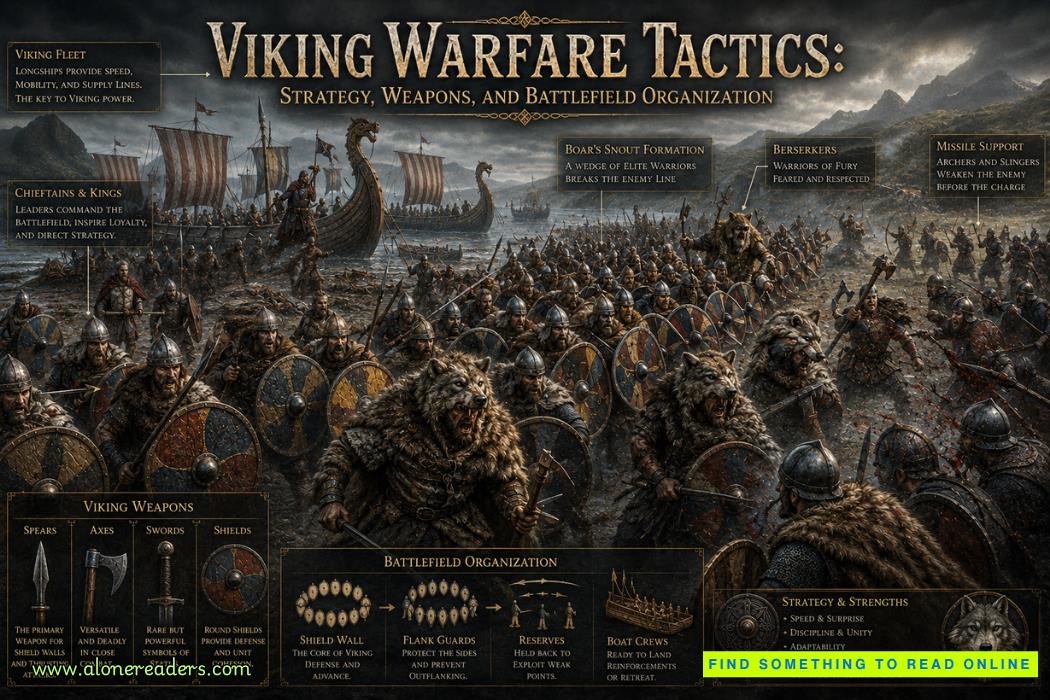

Viking Warfare Tactics: Strategy, Weapons, and Battlefield Organization

Viking Warfare Tactics: Strategy, Weapons, and Battlefield Organization

Women in the Viking Age: Exploring Their Roles, Rights, and Lasting Influence

Women in the Viking Age: Exploring Their Roles, Rights, and Lasting Influence

Orestes and the Rise of Military Strongmen in Rome: The Power Behind the Last Western Emperors

Orestes and the Rise of Military Strongmen in Rome: The Power Behind the Last Western Emperors

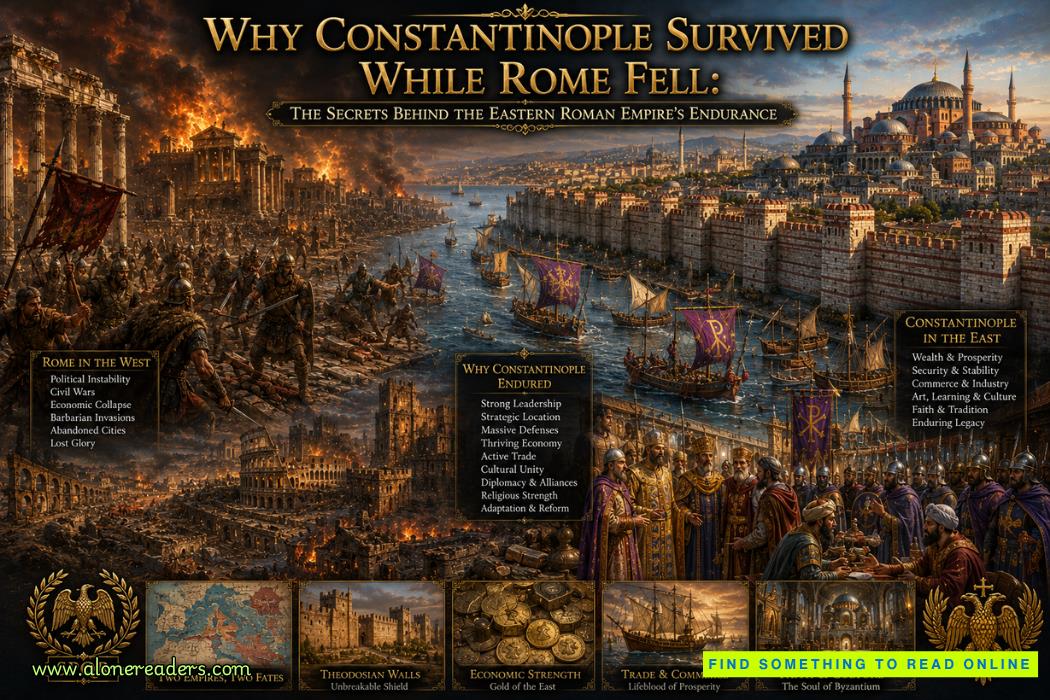

Why Constantinople Survived While Rome Fell: The Secrets Behind the Eastern Roman Empire's Endurance

Why Constantinople Survived While Rome Fell: The Secrets Behind the Eastern Roman Empire's Endurance